What Costs Eat Into HDB Sale Profit: 2026 Guide

- Pallipallisell

- Jun 23

- 8 min read

Your net HDB sale profit is defined as your sale price minus your outstanding loan, CPF refund with accrued interest, and all mandatory fees. Most sellers focus on the headline price and miss the full picture. What costs eat into HDB sale profit go well beyond agent commissions. They include CPF accrued interest, legal conveyancing fees, HDB administrative charges, and completion adjustments like property tax and Service and Conservancy Charges. Knowing each deduction before you list gives you a realistic cash figure to plan around. This guide breaks down every cost category so you can sell without surprises.

What costs eat into HDB sale profit the most?

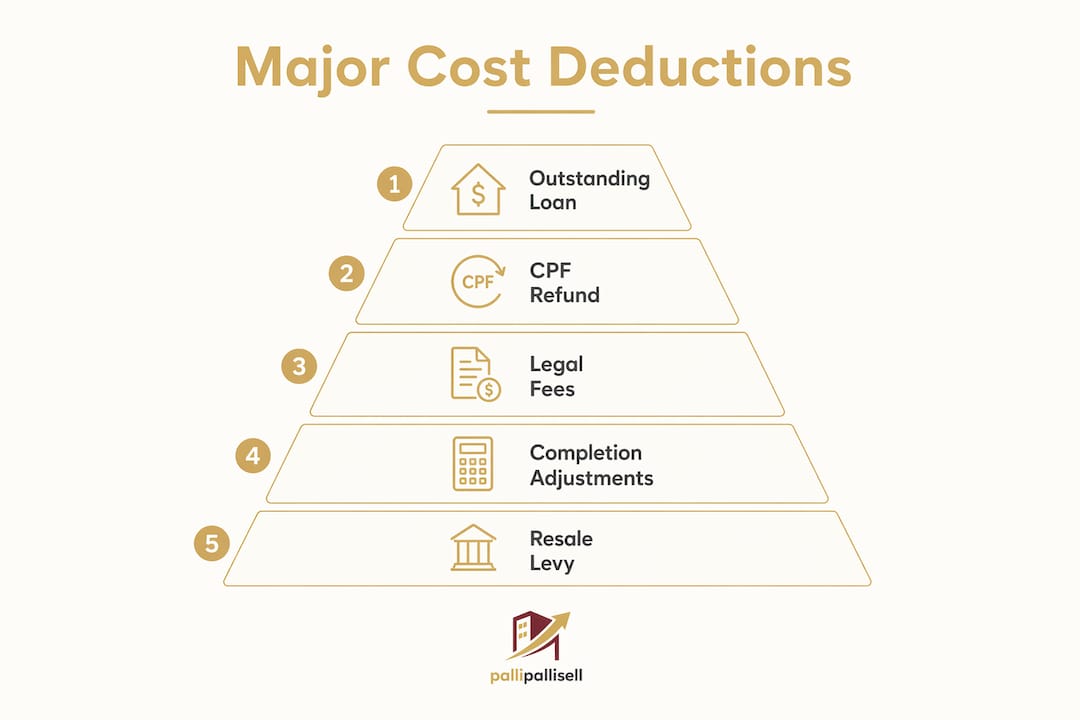

The net proceeds formula is straightforward: cash proceeds equal sale price minus outstanding loan, minus CPF refund with accrued interest and grants, minus all fees. Each element in that formula can be larger than sellers expect. The two biggest deductions are almost always the outstanding home loan and the CPF refund obligation.

Sellers who focus only on the sale price consistently underestimate mandatory deductions. A flat selling for $600,000 with a $200,000 outstanding loan and $150,000 in CPF refunds already has $350,000 committed before a single fee is paid. That leaves $250,000 in gross proceeds, which then shrinks further with legal, administrative, and completion costs.

Understanding this formula early changes how you price your flat and plan your next purchase. It also prevents the most common seller mistake: assuming a high sale price automatically means a large cash payout.

How do outstanding loans and CPF refunds reduce your cash?

The home loan repayment

Your outstanding home loan must be fully repaid at sale completion. There are no exceptions. If you owe $180,000 on your HDB loan or bank loan, that amount is deducted from your sale proceeds on the day of completion. You never receive that portion as cash.

The loan balance is predictable. You can request a redemption statement from HDB or your bank at any time. Budget this figure first before estimating your profit.

The CPF refund and accrued interest

The CPF refund is the deduction most sellers underestimate. CPF accrued interest compounds at 2.5% per year from the date of each withdrawal. This interest is not waived. It grows every year you hold the flat.

Here is a practical example. You withdrew $100,000 from CPF to fund your purchase 10 years ago. At 2.5% compounded annually, your CPF refund obligation is now roughly $128,000, not $100,000. That extra $28,000 goes back to your CPF Ordinary Account, not into your bank account. Longer hold durations increase this obligation significantly, which directly influences when selling makes financial sense.

The CPF refund also returns money to your CPF account, not as spendable cash. Sellers sometimes confuse a large CPF refund with a cash gain. The money is ring-fenced for retirement or your next property purchase.

Calculate your outstanding loan balance from your lender.

Request your CPF withdrawal statement from the CPF Board portal.

Use the HDB Sale Proceeds calculator to estimate accrued interest.

Subtract both figures from your expected sale price to get a realistic cash estimate.

Pro Tip: Run your CPF accrued interest calculation at least three months before listing. If the figure surprises you, you still have time to adjust your asking price or timeline.

What legal, conveyancing, and HDB administrative fees apply?

Even sellers who skip the agent still pay mandatory legal and conveyancing fees. These are non-negotiable costs of completing a legal property transfer in Singapore.

Legal fees for HDB resale range from roughly $1,800 to $5,000 depending on the law firm and flat size. HDB structures conveyancing fees by flat type, which gives you some predictability when budgeting. A 3-room flat will cost less in legal fees than a 5-room flat.

Fee Item | Typical Range | When Payable |

Legal/conveyancing fees | $1,800–$5,000 | At completion |

HDB resale application fee | At application | |

OTP processing fee | $120 | After OTP issued |

Caveat registration fee | $128.90 | At registration |

The HDB resale application fee is $40 for 1-room and 2-room flats and $80 for 3-room flats and larger. The $120 processing fee is triggered once the Option to Purchase is issued. These amounts are small individually but add up when combined with legal fees.

Get quotes from at least two law firms before committing to a conveyancer.

Confirm whether your chosen firm charges a fixed fee or a sliding scale by flat value.

Ask your conveyancer to itemize all disbursements upfront, including caveat registration.

HDB resale document endorsement must happen within HDB’s notice period. Missing this window delays your approval and can push back your completion date, affecting your cash flow timeline.

Pro Tip: Choose a law firm that specializes in HDB conveyancing. Specialists typically charge within the lower end of the $1,800–$5,000 range and process documents faster than general practice firms.

What completion adjustments reduce your final payout?

Completion adjustments are the costs that most sellers do not anticipate. They are not fees in the traditional sense. They are prorated charges settled on the day of completion.

Property tax is paid up to the date of completion. If you have already paid property tax for the full year, the buyer reimburses you for the unused portion. If you have not paid, the outstanding amount is deducted from your proceeds. Service and Conservancy Charges work the same way. Any arrears must be cleared before completion.

These amounts are typically modest, ranging from a few hundred to a few thousand dollars depending on your flat type and the time of year. But they reduce your net cash proceeds at settlement, and sellers who do not budget for them are caught short.

Clear all S&CC arrears at least one month before your expected completion date.

Check your property tax balance with IRAS before signing the Option to Purchase.

Ask your conveyancer to prepare a completion account statement so you see every adjustment in advance.

Factor in any outstanding town council charges that may appear at settlement.

How do renovation costs, resale levy, and indirect expenses affect your profit?

These costs do not appear in your sale proceeds statement. They reduce your overall financial gain from the sale, and ignoring them gives you a false picture of your net position.

Renovation and staging expenses are the most common indirect cost. Sellers often repaint, replace fixtures, or declutter before listing. These expenses can range from a few hundred dollars for minor touch-ups to several thousand for a full repaint and flooring refresh. They come out of your pocket before you receive a single dollar from the sale.

The HDB resale levy is a larger and more significant indirect cost. It applies when you sell your subsidized flat and then buy another subsidized HDB flat or Executive Condominium. The levy ranges from around $15,000 to $55,000 depending on your flat type. This amount is deducted from your CPF or paid in cash at the time of your next purchase, directly reducing the funds available for your upgrade.

Budget renovation costs separately from your sale proceeds calculation.

Check whether the resale levy applies to your next purchase before you commit to a sale price.

If you are upgrading to private property, factor in bridging loan interest as a real cost.

Opportunity costs like temporary rental accommodation between sale and purchase also reduce your net gain.

The resale levy surprises many sellers who plan to buy another subsidized flat. A seller who nets $300,000 in cash from their HDB sale but then pays a $50,000 resale levy has effectively netted $250,000 toward their next home.

Key Takeaways

Selling your HDB flat without an agent still leaves you with mandatory loan repayments, CPF refunds with compounding interest, legal fees, HDB administrative charges, and completion adjustments that together determine your true net cash proceeds.

Point | Details |

Net proceeds formula | Subtract outstanding loan, CPF refund with interest, and all fees from your sale price. |

CPF accrued interest | Compounds at 2.5% annually; a 10-year hold can add tens of thousands to your refund obligation. |

Legal and admin fees | Budget $1,800–$5,000 for conveyancing plus $40–$80 for HDB application and $120 for OTP processing. |

Completion adjustments | Property tax and S&CC arrears are settled at completion and reduce your cash payout. |

Resale levy impact | Ranges from $15,000 to $55,000 and applies when buying another subsidized flat after your sale. |

The cost most sellers realize too late

I have spoken with dozens of HDB sellers who walked into the process focused entirely on their asking price. Almost every one of them was surprised by the CPF accrued interest figure. It is the one deduction that grows silently while you hold the flat, and by the time you check it, the number can be significantly larger than you expected.

My honest advice: run your CPF calculation before you even decide to sell. If you have held your flat for 15 or more years and used substantial CPF funds, the accrued interest alone can reshape your financial plan. The HDB Sale Proceeds calculator is a practical starting point, but pair it with your actual CPF withdrawal history for accuracy.

Legal fees are the one area where you have some control. Conveyancing costs are structured by flat size, but law firms still have flexibility in their disbursements and service fees. Get two or three quotes. The difference between firms can be $500 to $1,000 on the same transaction. That is real money.

Timing also matters more than most sellers realize. Selling in the middle of a property tax year means your completion account will include a proration. Plan your completion date with your conveyancer to minimize unexpected adjustments. Transparent communication with your buyer on valuation and payment timelines also reduces last-minute surprises for both sides.

— Brandon

Selling your HDB flat without the commission cost

Skipping the agent commission is one of the clearest ways to protect your net proceeds. Traditional agent commissions run 1%–2% of the sale price, which on a $600,000 flat means $6,000–$12,000 out of your pocket. Pallipallisell offers a fixed fee of $688 to list and sell your HDB flat directly, giving you full control over your sale without the commission drain.

Pallipallisell’s platform lets you list your property and connect directly with buyers, so you handle negotiation and closing on your own terms. For sellers who want professional support without the full agent cost, check the fixed fee pricing to see exactly what you pay. When every dollar of your sale proceeds counts, a flat $688 fee beats a percentage commission every time.

FAQ

What is the biggest cost that reduces HDB sale profit?

The outstanding home loan and CPF refund with accrued interest are the largest deductions from your sale proceeds. Together they typically account for the majority of what is subtracted from your gross sale price.

Does skipping an agent eliminate all selling costs?

No. Sellers without agents still pay legal conveyancing fees, HDB administrative fees, and completion adjustments. Agent commission savings are real but do not remove these mandatory costs.

How is CPF accrued interest calculated?

CPF accrued interest compounds at 2.5% per year from the date of each CPF withdrawal used for the property. The longer you hold the flat, the larger the total refund obligation to your CPF account.

What is the HDB resale levy and who pays it?

The resale levy applies to sellers who buy another subsidized HDB flat or Executive Condominium after their sale. It ranges from around $15,000 to $55,000 depending on flat type and is paid from CPF or cash at the next purchase.

When do I pay legal and HDB administrative fees?

HDB application fees are paid at the time of resale application. Legal conveyancing fees are typically settled at completion. Your conveyancer will provide a completion account showing all charges before the final settlement date.

Recommended

Comments